As Florida temperatures have increased from spring to summer, so have local home insurance rates. Studies show that the average property insurance premium in Florida will increase by over a third in 2022. Why is this happening? Explore our guide to understand the reasons for increased costs, and see what you can do about them.

How Much Is Home Insurance in Florida?

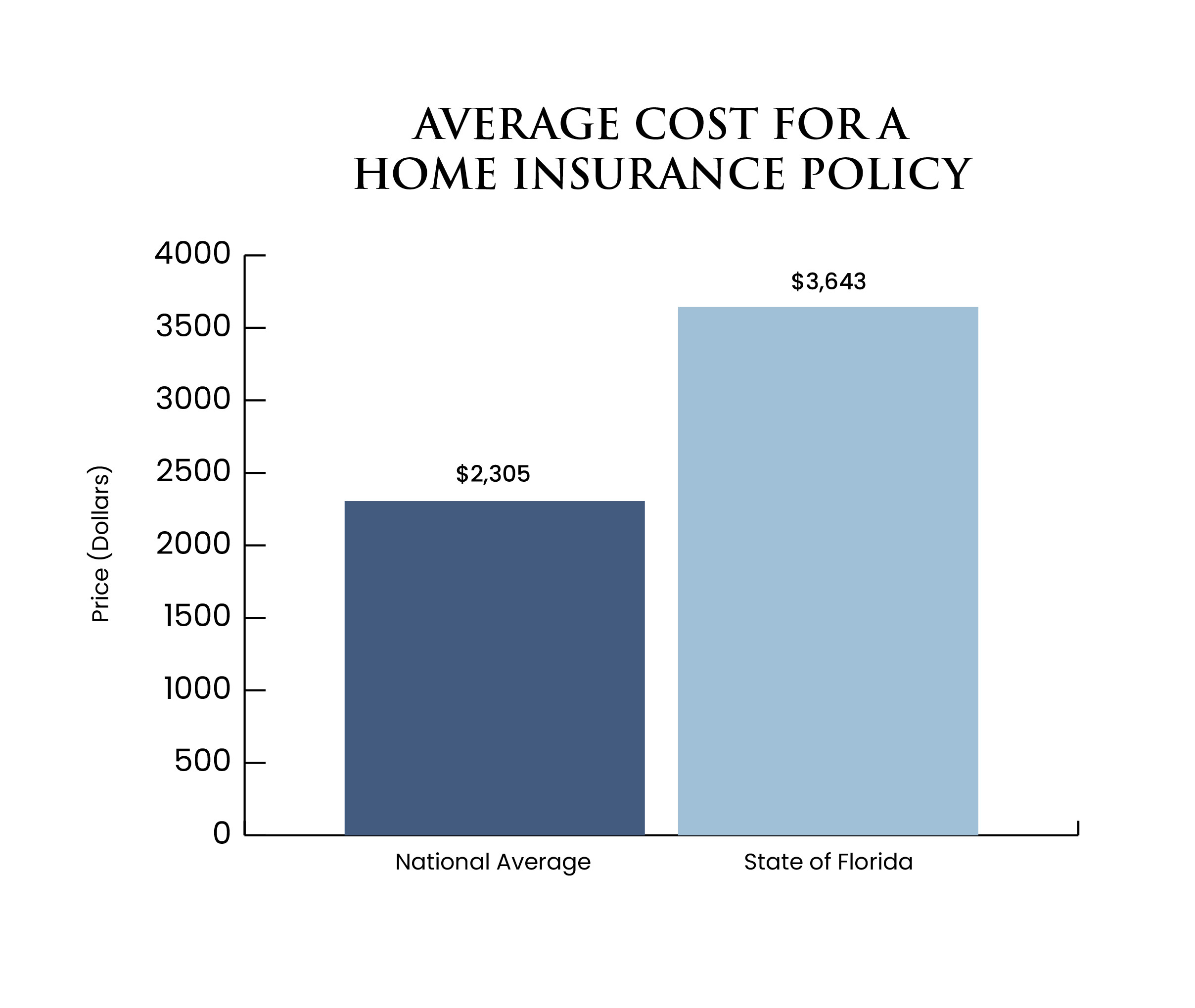

As of 2022, the average cost for a Florida home insurance policy is $3,643. This is significantly higher than the national average of $2,305, so it’s no surprise that Florida residents are complaining about costs.

As of 2022, the average cost for a Florida home insurance policy is $3,643. This is significantly higher than the national average of $2,305, so it’s no surprise that Florida residents are complaining about costs.

In addition to being higher than average, Florida insurance costs are also higher than historical averages. Last year, the average cost for insurance was around $1,600 to $2,000. Experts predict that rates will rise by 40% this year alone while national rates are predicted to rise just 4%. Some homeowners have even reported renewal rates of up to 50% more than their previous rates.

Keep in mind that these basic averages don’t give you the full picture, though. There is actually a lot of variety in Florida insurance rates. Part of this is simply due to the insurer you choose. For example, the same house could cost around $1,300 to insure through Tower Hill while Chubb would charge $2,400.

An even more important factor is location. Florida has a lot of low-lying land and oceanfront cities. These locations can be significantly pricier. For example, Miami-Dade residents pay roughly $450 per month on insurance while landlocked Polk County residents only pay around $180. For Florida residents in these pricier areas, the increase in home insurance costs has been even more devastating.

Why Is Home Insurance in Florida Rising?

There’s no single reason behind Florida’s bizarrely high insurance rates. Instead, multiple problems are combining all at once to cause soaring insurance costs.

Concerns About Catastrophic Claims

As climate catastrophes continue to increase, Floridians face more and more natural disasters. Rising sea levels, sinkholes, hurricanes, and tornados all regularly threaten Florida homes. The state ranks fifth in the number of federal disasters it has each year. In response to these issues, some insurance companies are insisting on higher rates. These higher costs help cover the increased risks associated with owning a home in Florida.

Increased Home Values

Florida’s housing boom has been a gold mine for many Florida residents. The combination of low interest rates and an increase in interested buyers has caused many people’s homes to double in value. Unfortunately, higher home values mean higher insurance rates. The cost to replace a home goes up when it has a higher value. This means you end up needing to pay for extra coverage to guarantee you can replace your home if a disaster strikes.

Issues With Home Insurance Fraud

In the past year, there has been a growing problem with insurance fraud. The main issue is predatory home repair companies. These companies tend to give homeowners a very inflated estimate for repairs. They then sue the insurance company to cover the repair costs, and the homeowners end up with increased rates.

Inflation

Part of the problem is simply due to inflation. In 2022, there has been a massive issue with inflated costs across the board. People are paying more for everything from gas to groceries to healthcare. Sadly, this is also affecting insurance rates. Companies are increasing their rates to keep up.

Rising Florida Home Insurance Displacing Some Florida Residents

Whatever the underlying cause, these high insurance rates are very problematic. For homeowners already struggling due to higher gas prices and grocery costs, having to pay an extra $1,000 dollars can be a huge hardship.

In some cases, high insurance costs can even cause homeowners to rethink their current homes. People who live on the coast can end up paying upward of $6,000 each year for insurance. Some of these people have reported that they are selling their houses and moving inland. For these residents, the prospect of saving tens of thousands of dollars over the course of their life is worth the move.

Ways to Lower Home Insurance Costs

Hate your insurance rates but don’t want to resort to moving out just yet? Try these tips to negotiate a lower rate for your homeowners’ insurance.

Improve Your Credit Score

Many homeowners are surprised to learn their credit score affects their insurance rates. Having a high score results in a lower premium because it tells the insurance company you’re a responsible person. To improve your credit score, you’ll need to do things like consolidating any debt, making regular payments on debt, and alerting the credit bureau to any fraud.

Enhance Your Home Security

Having a good home security system is a great way to protect yourself and decrease insurance costs. Since your policy usually covers theft or vandalism, insurance companies want to know your house is secure. Things like motion sensors, security cameras, and alarms can all reduce your policy.

Select a Higher Deductible

When choosing between insurance options, choose one with a higher deductible. This does mean you’ll have to pay more if something goes wrong, but it also gives you a lower premium. If possible, try setting aside the money you save by paying a high deductible. You’ll have some nice savings if nothing happens, and you’ll have funds to cover repairs if you run into any problems.

Stay With Your Current Provider

Many insurance companies let you lock in a rate for a set amount of time. Staying with your provider can also help you get loyalty discounts. Remember to shop around before deciding to stick with your provider, though. In some cases, you can save by taking advantage of another company’s deals for new customers.

Bundle Your Home Insurance Policies

If you’re in the market for new car insurance, too, consider getting an insurance bundle. This lets you pay a set amount to insure both your home and your automobiles. It can often allow you to get a significant discount on all your types of insurance.

Make Your Home Disaster-Proof

Insurance companies offer discounts for homeowners who make the effort to protect their homes. For example, if you get a wind-resistant roof, you can usually reduce your premium. This is a win-win for you and your insurance company. It reduces the chance of you making a claim, and if anything happens, it will be cheaper to repair.

Remove Items That Boost Your Premium

There are certain high-risk items that can cause your insurance company to increase your costs. Having a pool, trampoline, or playground is a major risk. They increase insurance costs because someone who gets hurt by the object can sue your insurance company. It may be worthwhile to rethink these sorts of add-ons if you need lower insurance.

Stay Informed on Market Trends

To make smart financial decisions, you need to be fully informed about Florida’s real estate market. Regularly checking the C.L.U.E. database is a great technique for staying up to date. This database is used by almost every insurance company. Its data provides valuable insight into market trends, insurance policies, and potential risks. Taking the time to look at your home’s C.L.U.E. report can help you take control of your finances.

Interested in learning other ways to improve your finances? Evergreen Investments is here to help. Contact us today to learn more about our real estate management services.

0 Comments